Table Of Content

- California climbers train for Mt. Everest from the comfort of their own beds

- Is now a good time to buy a house in California?

- What is a certified probate real estate specialist?

- Step 3: Save For A Down Payment And Closing Costs

- See What You Qualify For

- Preapproval document list

- Navigating West Virginia Home Inspections: A Guide for Homebuyers

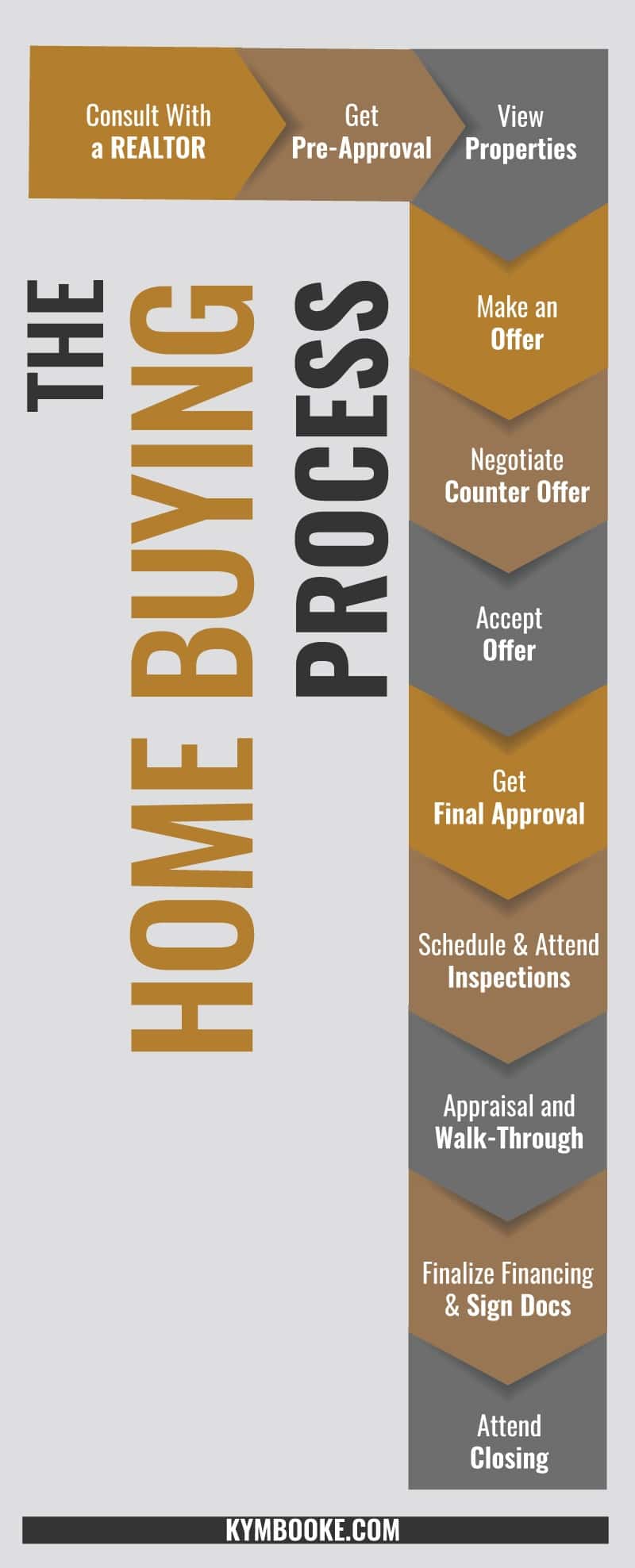

When you find a match, your agent can help you make an intelligent, informed offer. If your offer is accepted, a purchase contract is drawn and typically contains a good-faith deposit (“earnest money”) to show your commitment, usually between 1 percent and 3 percent of the sale price. Once the seller has accepted the offer, the earnest money will be deposited into an escrow account or held by the listing agent. Once the sale of the home has been completed, the earnest money you paid will be applied toward your closing costs. The credit score required to buy a house depends on your lender and the type of loan you’re taking out.

California climbers train for Mt. Everest from the comfort of their own beds

During a home inspection, an inspector will go through the home and look for specific problems. They’ll test electrical systems, make sure the roofing is safe, ensure appliances are working and more. After the inspection, the inspector will give you a list of problems they found in the home. Rocket Homes agents have proven track records of success and are at the top of their field, so you know you’ll get expert information. Use the Rocket Mortgage Home Affordability Calculator to get a rough idea of how much mortgage you can afford.

Is now a good time to buy a house in California?

This is also a good time to start looking for a solicitor or licensed conveyancer. Make purchases with your debit card, and bank from almost anywhere by phone, tablet or computer and more than 15,000 ATMs and more than 4,700 branches. Get transparent rates when you shop for title insurance all in one convenient place. Communication mostly happens over the phone between buying and selling agents, so you’ll likely be waiting on your agent for the latest status updates.

What is a certified probate real estate specialist?

Five Ways Buying and Selling a House Could Change - The New York Times

Five Ways Buying and Selling a House Could Change.

Posted: Mon, 18 Mar 2024 07:00:00 GMT [source]

The closing agent will ensure that all necessary parties are present at closing. The agent acts as a mediator between you and the seller and confirms that all required documents are signed. Once documents have been signed, the agent will ensure that all funds are paid and properly disbursed, including closing fees and escrow payments. At this point in the process, your lender will require the home to be appraised before they agree to release any funds. A home appraisal estimates how much a home is actually worth based on comparable sales in the area, market trends, public records and a comprehensive inspection of the property.

Keeping a monthly budget can help you stay on top of your mortgage and other costs, while taking care of your home over the long term. If not, keep looking – your new home, at a price you’re happy with, could be just around the corner. It may take some time, but when you find a property you want, deciding on the right price to offer can be exciting – and scary.

See What You Qualify For

The amount you’ll need for a down payment depends on your loan type and how much you borrow. If a down payment is required, you can buy a home with as little as 3% down (although putting down more has benefits). Qualifying for a loan isn’t a guarantee that your loan eventually will be funded—underwriting guidelines can shift, lender risk analysis can change, and investor markets can alter. Clients may sign loan and escrow documents, then be notified 24 to 48 hours before the closing that the lender has frozen funding on their loan program. Having a second lender that has already qualified you for a mortgage gives you an alternate way to keep the process on, or close to, schedule. During closing, the property title will pass from the seller to you.

While some home buyers might decide they want to buy on their own, having a trustworthy and reliable real estate agent can make things a lot simpler. If you meet only the minimum requirements, you may want to work on improving your credit score before applying for a mortgage, as this can get you access to better rates. In this article, we’ll introduce and walk you through each of the key steps to buying a house and walk you through them, so you’ll know exactly what you’re getting into and how to prepare. Although I received the $40,000 grant, I had to borrow the rest of the money from my lender.

Getting pre-approved initiates the mortgage process with a lender and tells you how much you can borrow. It also allows you to move faster when you’re ready to make an offer. It is important to get quotes from multiple lenders, rather than choosing the first mortgage lender you come across or even your current bank. Different lenders offer different mortgage options and rates, so research is key in finding the best rate for your homebuying goals.

How much house can you afford? Let’s figure it out

As your representative in the home purchase transaction, your real estate agent will look out for your best interests by finding homes that meet your criteria. These local market experts also get you showings, help you write offers and negotiate on your behalf. A real estate agent will help you locate homes that meet your needs and are in your price range, then meet with you to view those homes. Once you’ve chosen a home to buy, these professionals can assist you in negotiating the entire purchase process, including making an offer, getting a loan, and completing paperwork. A good real estate agent’s expertise can protect you from any pitfalls that you might encounter during the process.

Keep in mind that the larger the down payment, the more equity you’ll have, and the lower your monthly mortgage payments can be. By paying more upfront, you can save on interest and be less likely to pay private mortgage insurance (PMI). Be sure to weigh your options to choose the right down payment for you. A larger down payment may be great, but not if it means emptying your savings. Preapproval is different from prequalification, where the lender asks you a few questions and relies on your answers. With preapproval, you’ll actually provide documents and go through most of the checks required for a full mortgage application.

Make a list of your wants and needs, and rate them in order of importance. Once you select the best agent for you, they’ll look over your approval letter, discuss your budget and help you set your priorities. To calculate how much home you can afford, consider using the home affordability calculator below. Once you’ve determined how much you can afford, consider the lifestyle you want to maintain and leave yourself a cushion in case of emergencies. Don’t forget about factors like retirement, college funds and family vacations as you do your budget planning.

When that time comes, make sure you review your Closing Disclosure, which will outline the terms, final closing costs and any outstanding charges or fees included in your loan. Your lender will send the disclosure to you at least 3 business days before closing. Even if you’ve been preapproved for a loan, you should still write this contingency into your offer. If you don’t, you’ll find that you’re still on the hook for your earnest money deposit regardless of whether you’ve obtained a mortgage. The answer depends on how much you earn each month, how much you have in the bank, how much you must spend on other debts and how much houses cost in your particular part of the state. For example, in San Francisco — where median home prices are $1.54 million, according to CAR — the monthly mortgage payment on a median-priced home would be $7,787.

When looking at what is needed to buy a house, there are several steps in the process – from getting mortgage preapproval to house hunting to closing on your new home and, finally, getting ready to move in. While the process can take a lot of your time and effort, it can all be worth it to finally live in a home of your own. If you’re unable to find a buyer during that time, the home sale contingency will enable you to rescind your offer and reclaim your earnest money deposit without any recourse. Many sellers will refuse this contingency, but it’s still worth trying in most cases.

A common rule of thumb used by lenders in determining mortgage affordability is for the estimated mortgage payment to be no more than 28% of a borrower's monthly gross income. In deciding how big a loan to actually take, you’ll want to look at the house’s total cost, not just the monthly payment. You may also be able to take advantage of down payment assistance or closing cost assistance programs as a first-time buyer. These programs, which can be operated by state governments and nonprofit organizations, can provide you with funding to cover your down payment and closing costs in order to make your home ownership dream a reality. Perhaps even more important is having a real estate expert in your corner can provide some invaluable peace of mind.

If you take out a government-backed loan, you’ll typically need to pay an insurance premium or funding fee upfront. Financial health is another way of stating what one's financial condition is and involves savings, expenses, and ongoing income through employment. It also involves a person's credit score, which determines the ability to qualify for loans such as those for homes or new vehicles and the terms of the loans.

No comments:

Post a Comment